You’ve spent 30-plus years building. A distinguished career, a portfolio that’s grown through bull markets and survived the rough ones, a 401(k) that finally has some heft to it. You did the things you were supposed to do. You saved, reinvested, and stayed the course when it wasn’t easy.

And yet, once retirement appears on the horizon (close enough to actually be on the calendar instead of a far-off fantasy), something unexpected happens.

You find yourself running the numbers again. Wondering if you’ve missed something. Questioning what “ready” really means. It’s a bit like summiting a mountain and realizing that most climbing accidents don’t happen on the way up; they happen on the descent.

It’s more common than you might think. Because retirement planning is more complex than any single account balance can capture.

And having enough and being ready are not the same thing.

Having enough is a number. Being ready is a system. One that coordinates income, taxes, healthcare, timing, and the unpredictable realities of a retirement that could span 25 or 35 years.

If you don’t have a system to manage that complexity, then you are the system. And that’s a vulnerable position to be in.

This guide is designed to help you build that system, or at least understand what it should look like. We’ll work through the questions that determine success and sustainability in retirement, from spending and Social Security to taxes and healthcare, with the goal of helping you move from “I think I’m ready” to “I know I am.”

What Retirement Planning Really Means (And What It’s Not)

Ask ten people off the street what retirement planning means, and most will describe some version of the same thing: save enough money and invest it reasonably well.

That’s not retirement planning. That’s accumulation.

Accumulation is the first half of the game. True retirement planning is the second half. And the second half has different rules.

Here’s what retirement planning is not:

- Chasing a magic number (“I need $2 million and then I’m done”)

- Picking investments without accounting for income needs

- Timing the market

- Treating your 401(k) balance as a retirement readiness score

Here’s what it is:

- Coordinating income, taxes, healthcare, and timing so they work together instead of against each other

- Stress-testing decisions before they become irreversible because in retirement, many of the most consequential choices (when to claim Social Security, how to structure withdrawals, which Medicare plan to elect) don’t offer do-overs

- Turning a portfolio into a durable, flexible income plan that performs in both strong markets and weak ones

Think of it this way: a portfolio is a tool. A plan is a system. Systems put tools to work.

This is especially true for executives and long-tenure employees whose financial picture includes more than just a 401(k). Deferred compensation plans, restricted stock units (RSUs), non-qualified stock options, pension benefits — these instruments are often worth significant sums, and they come with their own tax treatment, vesting schedules, and timing considerations. How you sequence access to these assets can materially affect your tax bracket in the first decade of retirement.

In short, the purpose of retirement planning is to devise a personalized system that accounts for each of the variables (current and potential) in your life.

The Retirement Questions That Actually Matter

Most retirement anxiety concentrates around a few recurring fears. We hear versions of these regularly:

“Do I have enough to retire?” For many of the people we work with, the answer is more encouraging than they expected — including the timeline. It’s not uncommon to walk through someone’s full financial picture and find they can retire far sooner than they realized, sometimes by years. But that answer is only clear once you stop focusing on a balance and start focusing on a plan.

“What happens if markets crash early?” This is the right question. Sequence-of-returns risk (the danger of retiring into a market downturn) is one of the most consequential and underappreciated threats in retirement planning. Two portfolios with the same average returns can look vastly different after 25 years just based on the order of those returns.

Read more: Will My Savings Last Throughout My Retirement?

“How much can I realistically spend without running out?” More than you might think, if the plan is designed thoughtfully. But “how much” is less important than how you structure the spending — with guardrails, flexibility, and a realistic sense of how expenses tend to evolve over time.

“Am I missing any tax traps I won’t see until it’s too late?” Possibly. The years between retirement and age 73 represent a rare and often underused window for tax planning. How you manage that window (e.g., Roth conversions, strategic withdrawals) can be worth hundreds of thousands of dollars over a full retirement.

“Should I work one more year, or is that just fear talking?” This is the most personal question on the list. Sometimes working longer is a sound financial decision. Sometimes it’s anxiety dressed up as prudence. A good retirement plan helps you tell the difference.

These aren’t rhetorical questions. The rest of this page is dedicated to answering them.

Understanding Your Retirement Spending (Before You Fixate on Account Balances)

Your account balance gets a lot of attention. But what about your spending rate?

Your spending rate is the most controllable lever in retirement planning. It determines how quickly you draw down your retirement savings, how long your portfolio lasts, and how much flexibility you have in response to one of life’s many inevitable curveballs.

To illustrate the stakes, if you retire with a $1 million portfolio, withdraw $5,000 per month, and assume a 7% annual return with 3% inflation, your savings last roughly 26 years. Increase that withdrawal by just $600 per month — a few extra dinners out, a new car payment, a few more golf rounds — and the lifespan of your portfolio drops by more than four years. A modest, seemingly inconsequential adjustment with a significant long-term consequence.

Rather than fixating on a precise monthly budget, the more durable approach is to establish retirement income guardrails: a dynamic withdrawal framework that expands or contracts spending based on portfolio performance and market conditions.

If markets perform well, your guardrails allow spending to increase modestly. If they struggle, you pull back — not drastically, but enough to preserve the portfolio’s longevity.

This approach tends to produce more years of financial comfort than rigid, rules-based strategies. And importantly, it gives you a framework for spending confidently, so you’re not second-guessing every trip or home repair against the imagined toll it takes on your financial future.

The Reality of Retirement Spending Patterns

Retirement calculators are very useful tools, but there’s a flawed variable that they hinge on: they assume spending is more or less linear.

It isn’t.

Retirement spending, for many retirees, is more variable than most projections assume. In the early years, spending typically peaks; this is when the freedom to travel, pursue hobbies, and invest in experiences is both available and energizing. In the middle years, spending usually moderates as routines settle in. Later in retirement, costs tend to rise again as healthcare and care-related needs become more prominent.

Treating retirement income as a single flat number across three decades ignores this natural arc. A well-constructed retirement plan accounts for it — allowing for higher discretionary spending early, appropriate reserves in the middle years, and a realistic budget for healthcare in the later stages.

For executives with deferred compensation payouts landing in early retirement, this spending arc deserves extra attention. A large taxable distribution in year two of retirement, layered on top of early portfolio withdrawals and other income, can push you into territory you didn’t anticipate. Planning the timing of those payouts and how they interact with spending needs is imperative.

Turning Savings Into Income You Can Rely On

The 4% rule is one of the most cited guidelines in retirement planning, and for good reason. Developed by financial planner William Bengen in the 1990s after analyzing thousands of retirement portfolios through bear markets, it holds that retirees can withdraw approximately 4% of their portfolio annually, adjusted for inflation, and sustain that income for at least 30 years.

In 150 years of market history, there has never been a 30-year stretch in which the 4% rate would cause a retiree to run out of money.

That’s a sterling track record. But it’s also a floor, not a formula.

The 4% rule assumes a fixed 50/50 portfolio allocation. It doesn’t account for pensions, Social Security timing, large one-time expenses, or the tax treatment of different account types. For retirees with significant assets in tax-deferred accounts, delaying Social Security, or managing executive compensation payouts, the real withdrawal rate may look quite different — sometimes sustainably higher, sometimes requiring more caution.

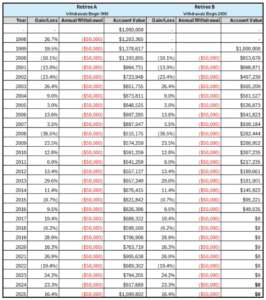

The more important concept is sequence-of-returns risk: the reality that not all market years are equal, and that the order in which returns happen matters enormously in retirement.

Consider two retirees with identical portfolios, identical withdrawal rates, and identical average returns over 20 years, but one retires in 1998 (enjoying two strong years before the dot-com crash) and the other retires in 2000 (stepping directly into the downturn). Same averages. Completely different outcomes. One portfolio not only survives and recovers — it exceeds its original value, even with annual withdrawals. The other depletes before the retiree’s 81st birthday.

This is why retirement income planning isn’t as simple as picking and sticking to a static withdrawal rate. Withdrawals should be structured so that early-year losses don’t permanently compromise the portfolio’s longevity. Diversification across asset types and income sources is the first line of defense; guardrails, cash reserves, and deliberate sequencing across account types are the mechanisms that sustain it.

Coordinating Income Sources

Most retirees draw from several income streams, each with its own timing, tax treatment, and strategic role:

- Social Security benefits: guaranteed, inflation-adjusted, and highly dependent on when you claim (more on this shortly)

- Withdrawals from retirement accounts: traditional IRAs, Roth IRAs, and 401(k) plans, each taxed differently and subject to different rules around timing and required distributions

- Taxable brokerage accounts: flexible, no RMD requirements, and potentially taxed at favorable long-term capital gains rates

- Pensions or annuities: guaranteed income that reduces reliance on portfolio withdrawals and mitigates longevity risk

- Deferred compensation or RSU distributions: common for Fortune 500 executives, often taxed as ordinary income and requiring careful scheduling around other income events

- Part-time work or consulting: more common than it used to be, and worth accounting for in early retirement income modeling

Whatever combination you hold, it’s important to orchestrate them so that your combined income is tax-efficient, resilient across market conditions, and flexible enough to accommodate the unexpected.

Read more: What Is the Best Way to Withdraw My Savings?

Managing Taxes Across Your Retirement Timeline

During your working years, taxes are almost invisible. Your employer withholds them automatically. You file in April, maybe owe a bit or receive a refund, and move on. It’s routine.

Retirement breaks that routine entirely.

Without a paycheck, there’s no withholding. Every financial decision — when to take a distribution, how much to pull from which account, when to sell an appreciated asset — carries a tax consequence. And because income flows from multiple sources, with different tax implications, the combined effects can be significant and surprising.

Social Security is a prime example. Many retirees are surprised to learn their benefits are taxable. If your combined household income exceeds $44,000, up to 85% of your Social Security benefits are taxed at your marginal rate. In Minnesota specifically, one of only a handful of states that taxes Social Security income, joint filers with provisional income above $108,320 can see up to 85% of their benefits taxed at the state level as well.

RMDs add another layer. Starting at age 73, the IRS requires withdrawals from traditional retirement accounts whether you need the money or not. A large RMD layered on top of Social Security, investment income, and any remaining deferred compensation can push you into a higher tax bracket, increase the taxable portion of your Social Security benefits, and trigger Medicare IRMAA surcharges that raise your premiums.

Coordinating Account Types

Most retirees have assets spread across three types of accounts:

| Account Type | Examples | Tax Treatment |

| Investment Accounts

(Taxable) |

Brokerage accounts, stocks, ETFs, mutual funds | Capital gains taxes apply on any profits when selling assets. Tax rates on long-term capital gains range from 0% to 20% depending on your income and filing status. Short-term capital gains (assets sold within a year of taking ownership) are taxed as ordinary income. |

| Traditional Accounts (Tax-Deferred) |

401(k), IRA, SEP IRA, SIMPLE IRA | Withdrawals are taxed as ordinary income. Required minimum distributions (RMDs) begin at age 73. |

| Roth Accounts (Tax-Free) |

Roth 401(k), Roth IRA | Withdrawals are tax-free if the account has been open for at least five years. No RMDs for Roth IRAs. |

The order in which you draw from these accounts has a direct impact on your lifetime tax bill. A conventional approach starts with taxable accounts (to allow tax-advantaged savings to continue growing), then moves to tax-deferred accounts, and preserves Roth accounts for last. But this isn’t a universal prescription. Proportional withdrawals across account types, Roth conversions during lower-income years, and strategic use of long-term capital gains rates can all reduce total tax liability depending on your situation.

Executives, specifically, may have large concentrations in tax-deferred accounts, accumulated through decades of 401(k) contributions. As a result, the risk of a future RMD spike deserves early attention. The window between retirement and age 73 is often the best opportunity to convert a portion of pre-tax savings into a Roth IRA at lower tax rates. Every dollar converted in that window is a dollar that will never become a forced, taxable distribution.

The tax advantages of the Roth IRA — tax-free growth, tax-free withdrawals, no required distributions — are hard to replicate elsewhere. Used strategically, they can serve as a meaningful tax buffer for both you and your heirs.

Required Minimum Distributions and Timing Risk

RMDs can be a disruptive force in an otherwise well-designed retirement plan.

The logic is simple: the government allowed you to defer taxes on your 401(k) and IRA contributions for decades. At age 73, it wants its share. You’re required to take a minimum withdrawal each year, calculated based on your account balance and IRS life expectancy tables. The amount grows as a percentage of your balance over time.

The risk is that those forced withdrawals arrive at the worst possible moment. Namely, when your income from other sources is already high, when markets have recovered and your balances are elevated, or when the added income triggers Medicare premium increases you didn’t budget for.

The antidote is proactive planning well before age 73. Strategic withdrawals from tax-deferred accounts in your early retirement years, Roth conversions timed to stay within favorable brackets, and qualified charitable distributions are all tools that reduce future RMD exposure.

The window to act is often narrower than retirees expect. Once RMDs begin, flexibility withers considerably.

Read more: The Retiree’s Tax Planning Guide: How to Keep More of Your Money

Social Security: An Important (and Permanent) Decision

Social Security is a powerful income lever in retirement. It’s also easily mishandled.

The usual mistake is treating the claiming decision as administrative rather than strategic — picking an age, filing the paperwork, and moving on.

For most retirees, Social Security is the only income source in retirement that is guaranteed for life, protected against inflation through automatic cost-of-living adjustments, and largely uncorrelated with stock market performance. The timing of your decision impacts everything else in your financial plan.

The Basics of Claiming

Your full retirement age (FRA) is the age at which you receive 100% of your calculated benefit and is typically 66 or 67, depending on your birth year. Claiming before your FRA permanently reduces your monthly benefit by as much as 30%. Delaying beyond your FRA increases it by approximately 8% per year until age 70, at which point retirement benefits max out at 124% of your FRA amount.

For someone with a $3,000/month FRA benefit, delaying from 67 to 70 adds roughly $720 per month — for life, adjusted annually for inflation. Over decades of retirement, that’s a substantial difference in lifetime income.

The Coordination Dimension

Social Security claiming is also a tax and portfolio decision.

Claiming earlier reduces pressure on portfolio withdrawals in the first years of retirement, which can help portfolios recover from early-year downturns. But it also locks in a lower monthly benefit permanently, increases the long-term tax burden on Social Security income, and may reduce survivor benefit protection for a spouse.

By delaying Social Security, you’ll likely draw more from your portfolio in early retirement, which increases sequence-of-returns exposure. But it also allows for Roth conversions and strategic withdrawals from tax-deferred accounts at lower rates during those years, reducing future RMD exposure and potentially lowering lifetime taxes.

For married couples specifically, the claiming decision is even more layered. Spousal benefits allow a lower-earning spouse to receive up to 50% of the higher earner’s benefit. Survivor benefits allow a widowed spouse to inherit up to 100% of the deceased spouse’s benefit — but only at the level the deceased had locked in. That’s why, in many households, it makes sense for the higher earner to delay as long as possible: they’re not just maximizing their own income, they’re protecting their spouse’s financial security for the rest of their life.

There is no universally right answer. The optimal claiming strategy depends on your health, your portfolio withdrawal needs, your spouse’s situation, your tax bracket, and the broader income picture.

Read more: When Is the Best Time to Claim Social Security?

Estate Planning: Taking Care of Your Loved Ones

Estate planning has an image problem. People associate it with drafting a will, signing some forms, and filing them away.

Except estate plans that gather dust in folders don’t protect families.

A retirement plan and an estate plan are deeply intertwined. How you withdraw from your accounts affects what’s left for heirs. Which accounts pass to beneficiaries and whether those assets are pre-tax, tax-free, or taxable directly affects the after-tax value of what your family receives. Roth conversions you complete today may primarily benefit your children or grandchildren decades from now.

Common Gaps

Even among financially sophisticated near-retirees and retirees, certain estate planning vulnerabilities appear again and again:

Outdated beneficiary designations. Beneficiary designations on 401(k) plans, IRAs, life insurance policies, and annuities override whatever your will says. If you remarried, had children, or experienced the death of a previously named beneficiary and didn’t update these designations, the consequences can be significant and irreversible after the fact.

Taxable accounts passing inefficiently. Assets in traditional retirement accounts pass income taxes along to heirs when they withdraw. Assets in taxable brokerage accounts, on the other hand, typically receive a step-up in cost basis at death, meaning heirs pay little or no capital gains tax on appreciation that occurred during your lifetime. Understanding which account types to spend from during retirement versus which to leave as inheritance can drastically affect the tax efficiency of your estate.

No clear plan for incapacity. A will addresses what happens when you die. A durable financial power of attorney addresses what happens if you can’t manage your finances. A healthcare directive addresses medical decision-making. Without these instruments in place, family members may be powerless to act on your behalf at an already emotionally charged time.

Integrating Legacy Planning Into Retirement Decisions

Minnesota adds its own layer of complexity. Unlike most states, Minnesota imposes a state estate tax in addition to the federal one. The state exempts the first $3 million of an estate’s value; anything above that is taxed on a graduated scale from 13% to 16%.

Strategic gifting can help address this over time. In 2026, the IRS allows individuals to gift up to $19,000 per recipient per year without triggering gift taxes or reducing the lifetime exemption. Couples can combine that amount to $38,000 per recipient annually — a tactical transfer approach for those with children or grandchildren they want to support.

Charitable giving vehicles, such as donor-advised funds, charitable remainder trusts, and qualified charitable distributions from IRAs, offer additional tools for reducing taxable estate values while supporting causes that matter to you.

The overarching point is that estate planning is a process, not an event. It requires periodic review as account values shift, tax laws evolve, family circumstances change, and retirement decisions are made. Treating it as a one-time task is how gaps develop.

How Do I Plan My Legacy and Protect My Family’s Future?

Healthcare Planning: Don’t Underestimate the Unpredictable

Healthcare is one of the most underestimated (and unpredictable) expenses in retirement. A 65-year-old retiring today should plan for approximately $172,500 in out-of-pocket medical expenses over the course of retirement, even with Medicare coverage in place.¹ That figure doesn’t include extended long-term care, which is its own financial category.

Medicare eligibility doesn’t begin until age 65. That creates an immediate planning question for many near-retirees: what do you do about health insurance in the meantime?

If you retire at, say, 62 or 63, that’s two or three years of potentially expensive individual market coverage. This cost should be factored into early retirement income modeling. It’s not unusual for pre-Medicare health insurance to run $1,500 to $2,500 per month for a couple, depending on age and coverage level.

Once Medicare begins, the decision tree branches. Original Medicare (Parts A and B) covers hospital and outpatient care but leaves notable gaps — no dental, no vision, no routine long-term care, and a 20% coinsurance requirement on most services after the deductible. To fill those gaps, most retirees elect either a Medigap supplemental policy (which works alongside Original Medicare) or a Medicare Advantage plan (Part C, a private plan that replaces Original Medicare with typically bundled coverage including Parts A, B, and D).

Both paths have tradeoffs:

- Medigap offers greater provider flexibility and more predictable out-of-pocket costs, but typically carries higher monthly premiums

- Medicare Advantage usually has lower premiums and often bundles dental, vision, and fitness benefits — but operates through networks, which can limit provider choices

One path isn’t better than the other. The right plan depends on your health needs, budget, and preference for flexibility versus cost predictability.

One additional consideration: IRMAA surcharges. Medicare Part B and Part D premiums increase once your income surpasses certain thresholds — $109,000 for individual filers, $218,000 for married filers filing jointly, as of 2026 guidelines. These surcharges can add thousands of dollars to annual healthcare costs, another reason why income coordination in the years before and during Medicare enrollment has direct consequences for your bottom line.

It’s also worth noting that healthcare costs vary significantly depending on where you live. Urban markets, regions with physician shortages, and areas with fewer competing health systems tend to have higher costs for the same services. If you’re considering relocating in retirement (or staying put in a higher-cost area), that should factor into your healthcare planning assumptions.

Read more: What State Should I Retire In? Tax, Lifestyle, and Healthcare Factors to Consider

Long-Term Care Planning

Research has found that 70% of adults who reach age 65 will need some form of long-term care in their lifetime.² One in five will need it for five or more years.³

And yet it’s routinely overlooked in many retirement plans.

Long-term care encompasses a range of services: in-home assistance, adult day care, assisted living, and skilled nursing facilities. In Minnesota, a private room in a nursing home runs over $135,000 per year on average.⁴ In-home care for a health aide can cost more than $7,000 per month.⁵

Medicare covers very little of this. It handles short-term skilled nursing following a hospital stay, but it does not cover ongoing, custodial care — the type most retirees would actually need. Medicaid does cover long-term care, but only after nearly all personal assets have been depleted.

The primary options for managing long-term care risk are:

- Long-term care insurance: dedicated policies covering a range of care settings, with premiums that vary significantly based on age, health, and coverage terms. Policies purchased in your late 50s or early 60s are generally more affordable and flexible than those purchased later.

- Hybrid life/LTC policies: life insurance or annuity products with a long-term care rider, which means if LTC coverage is never used, a death benefit passes to heirs instead.

- Self-insuring: funding potential care costs from existing assets. This can be an appropriate route for those with high net worth and sufficient liquidity.

You may have one additional option. If you’re delaying Social Security, deferring a pension, or incorporating annuities into your plan, these can act as a “soft” LTC policy — one that doesn’t require medical underwriting.

These income sources follow a longevity curve, meaning the older you are when you claim, the higher your payout. As a result, you can strategically time these benefits to provide additional financial stability in your later years. They don’t outright replace the coverage and features of a LTC policy, but they at least establish a guaranteed income floor.

Long-term care is not a remote risk. It’s a planning variable that belongs in your retirement strategy, with an honest estimate of potential costs and a realistic approach to funding them.

Read more: How Should I Plan for Health Care Costs and Long-Term Care?

Working With a Financial Advisor: What to Actually Expect

Many of the soon-to-be retirees we work with have a lot in common.

They’ve judiciously managed their personal finances for decades. They’ve consistently contributed to their 401(k), prioritized saving and investing, and generally felt like they had a handle on things. That was enough, for most of their careers.

But as retirement crests the horizon, something changes. The weight and implications of the decisions start to feel heavier, more permanent. And a lingering question creeps in that no spreadsheet could quite answer: Have I actually been making the right decisions?

That’s usually the moment someone seriously considers finding an advisor: they’ve reached the point where the cost of being wrong — and the cost of not knowing they’re wrong — is too high to ignore.

In many cases, there’s a second layer, too: skepticism. A lot of near-retirees have had at least one experience with a financial professional who seemed more interested in selling something than in giving honest guidance. Calls that only came when there was a product to pitch. It leaves an indelible impression, and it’s one of the main reasons people wait longer than they should to seek out genuine guidance.

It’s a fair reason to be cautious, and a fair reason to ask how an advisor gets paid before anything else.

Pine Grove Financial Group is a fee-only advisory firm, which means we don’t earn commissions on what we recommend. No products to push. No incentive to steer you toward anything other than a plan that works for your situation.

What does working together actually entail?

A comprehensive review of your financial standing. Account balances, income sources, tax exposure, healthcare costs, executive compensation structures, beneficiary designations, and estate documents. The goal is to uncover gaps before they turn into expensive surprises.

Stress-testing hypotheticals and variables. Running your plan through adverse scenarios (e.g., a significant market downturn in year two, an extended period of elevated healthcare costs, higher-than-expected taxes on deferred distributions) helps identify the vulnerabilities in your plan while you still have time to address them.

Coordinated decision-making. When to claim Social Security, which accounts to draw from first, whether to do Roth conversions, how to structure executive compensation payouts, how to title assets for estate purposes — these decisions influence one another. Good financial planning treats them as a system.

A plan that doesn’t require you to run it alone. Retirement is an unusual period of life, genuinely unlike anything that came before it. For the first time in decades, income doesn’t arrive on its own; you have to manufacture it, deliberately, from a collection of assets that need to last 25 or 30 years while also funding a life you’ve been looking forward to. The freedom that comes with that is real — and easy to underestimate until you’re living it, suddenly in command of your time in a way that’s equal parts liberating and disorienting. A good advisory relationship means you’re not trying to think through all of it alone, without a frame of reference, every time something shifts.

One thing worth saying plainly: trust is paramount. This is your financial life — information you don’t share with just anyone. You should feel confident in who you’re working with before you share it. That confidence should come from transparency, from a genuine sense that the advisor’s interest is aligned with yours, and from the work itself: the rigor of the analysis, the honesty of the answers, and the willingness to show you the variables that make the plan hold up even when circumstances change.

If you’re within five years of retirement, or if you’ve recently retired and want a second opinion on your current plan, we’d welcome the conversation. The first step is simply finding out where you stand.

¹Fidelity 2025 Retiree Health Care Cost Estimate

²Jackson National Life Insurance Company, Security in Retirement (2025)

³ACL, “How Much Care Will You Need?”

⁴Senior Living, Nursing Home Costs in 2026

⁵A Place for Mom, “Cost of Long-Term Care and Senior Living”

See If You're a Good Fit

Your responses go directly to a senior member of our team, who’ll guide the next steps toward a personal conversation. No automation. No sales pressure.