If you’re like most of the workforce, you’re used to paychecks arriving like clockwork, funding your lifestyle, covering bills, and offering the security of financial consistency. Retirement throws a wrench in this structure — how do you recreate a steady, predictable income stream from your savings?

Unlike Social Security, which calculates your guaranteed monthly payments for you, your personal savings and investments require manual oversight to not only support your retirement but also withstand obstacles like inflation, market downturns, and tax liabilities.

In this article, We’ll break down how to approach withdrawal strategies, explore the tax implications of different accounts, and show you how to structure withdrawals for long-term sustainability.

Why Withdrawal Strategies Matter

While Social Security provides a lifetime income stream, your personal savings don’t come with the same guarantee. Unfortunately, almost half of all American households are at risk of running out of savings during retirement, according to Morningstar research.

That’s why withdrawal rates matter. Since the average age of retirement is 65 for men and 63 for women, you may be relying on your investments for 20 to 30 years or so. A calculated withdrawal strategy allows you to accomplish three life-changing goals in this time frame:

- Generate a reliable income stream

- Minimize your tax burden over time

- Preserve your portfolio longevity

Fortunately, there are proven methods to do so.

How Taxes Impact Your Withdrawals

The first step to strategic withdrawals is to minimize your tax burden. Most retirees have three sources of savings to draw from, each of which is taxed differently.

| Account Type | Examples | Tax Treatment |

| Investment Accounts (Taxable) | Brokerage accounts, stocks, ETFs, mutual funds | Capital gains taxes apply on any profits when selling assets.

Tax rates on long-term capital gains range from 0% to 20% depending on your income and filing status.

Short-term capital gains (assets sold within a year of taking ownership) are taxed as ordinary income. |

| Traditional Accounts (Tax-Deferred) | 401(k), IRA, SEP IRA, SIMPLE IRA | Withdrawals are taxed as ordinary income. Required minimum distributions (RMDs) begin at age 73. |

| Roth Accounts (Tax-Free) | Roth 401(k), Roth IRA | Withdrawals are tax-free if the account has been open for at least five years. No RMDs for Roth IRAs. |

Some retirees also have money in a Health Savings Account (HSA). These accounts allow you to withdraw funds tax-free for medical expenses.

Or, once you turn 65, you can withdraw funds for any reason and pay taxes at your ordinary income tax rate.

|

Tip: If you withdraw money from traditional or Roth accounts before age 59 ½, you’re subject to an additional 10% tax. There are options for early retirees to avoid penalties, including withdrawing only Roth IRA contributions or taking advantage of the “rule of 55” for 401(k)s. Talk to a wealth advisor for more details if early retirement is in the cards. |

Managing Taxes Through Smart Withdrawals

Taxes on withdrawals could be as low as 0% or as high as 37% depending on your tax bracket and withdrawal strategy. In other words, it pays (quite literally) to be cautious about when and how you access your funds.

As you develop your strategy, there are two goals to keep in mind:

#1: Stay below the Medicare IRMAA thresholds.

Your Medicare Part B and D premiums increase once your income surpasses certain limits. These higher premiums, known as income-related monthly adjustment amounts (IRMAA), take effect when your income exceeds:

- $106,000 for single tax filers

- $212,000 for married tax filers

If you coordinate a Roth conversion strategy within these IRMAA limits, you can achieve a nice two-for-one bonus: you’d not only keep health care premiums at the lowest level but also save money on taxes in the process.

Even if you were to exceed these limits, in many cases, the savings from a Roth conversion outweigh the increase in premium cost.

#2: Minimize the tax impact of RMDs.

Starting at age 73 (or 75 beginning in 2033), you’re required to withdraw a certain amount from your traditional retirement accounts. These RMDs count as taxable income, which could:

- Push you into a higher tax bracket

- Increase Social Security taxes

- Trigger Medicare IRMAA surcharges

|

Tip: MAGI is your adjusted gross income from Line 11 of your 1040 tax form, plus tax-exempt interest income and untaxed foreign income. |

Required Minimum Distributions: What You Need to Know

If you have money in pre-tax retirement accounts like a 401(k) or traditional IRA, you’ll eventually have to start making withdrawals, whether you need the money or not. RMDs are the government’s way of ensuring your tax-deferred savings are eventually taxed.

The bigger problem, however, is that RMDs can have unintentional consequences:

- Higher taxable income. You may have to withdraw more than you need, pushing you into a higher tax bracket.

- Higher Social Security taxation. Higher income from RMDs could make up to 85% of your Social Security benefits taxable, which just adds insult to injury since you’re already facing a bigger bill.

- Higher Medicare premiums. If your MAGI exceeds certain thresholds, you could trigger higher Medicare Part B and Part D premiums.

Fortunately, There are strategies to minimize the impact of RMDs. You could:

- Start early withdrawals. Taking smaller withdrawals before RMDs begin can help spread out your tax burden and prevent a sudden spike in income.

- Convert to a Roth IRA. Roth conversions allow you to move money from pre-tax accounts to a Roth IRA (where future withdrawals are tax-free). This works best in lower-income years, as it comes with an upfront tax bill.

- Use qualified charitable distributions. If you’re charitably inclined and at least 70 ½, you can donate up to $100,000 per year directly from your IRA to a qualified charity, completely avoiding taxes on that withdrawal.

For many retirees, a Roth conversion during a lowerincome year is the best option to provide more flexibility — and more tax-free income — later in life.

However, If you don’t want to pay a large tax bill on converted funds, early withdrawals may be the better choice.

The Sequence of Withdrawals — What Comes First?

Now that you understand why the sequence of withdrawals is important, let’s take a look at two different approaches to structuring withdrawals.

1. Conventional wisdom: Taxable → Traditional → Roth

A widely accepted withdrawal strategy follows this order:

- Start with taxable accounts

- Move to traditional (pre-tax) accounts

- Tap Roth accounts last

Step 1: Withdraw from taxable accounts first.

- Allows tax-advantaged accounts (Traditional IRA, 401(k), and Roth IRA) to keep growing.

- Enables tax-efficient withdrawals, especially if selling investments at long-term capital gains rates (which could be as low as 0%).

- Ideal for early retirees under age 59½, since taxable accounts have no early withdrawal penalties.

- Keeps taxable income low by delaying Social Security and RMDs.

Step 2: Tap traditional (pre-tax) accounts next.

- Preserves your Roth accounts and allows these funds to continue compounding, which translates to more money you can withdraw tax-free later in retirement.

- Allows you to space out your withdrawals if you retire at a younger age, so your RMDs are smaller.

- Balances withdrawals to prevent sudden jumps in income that could increase Medicare premiums or Social Security taxes.

Step 3: Use Roth accounts last.

- Allows more time for Roth accounts to grow tax-free.

- Unlocks flexibility since Roth IRAs have no RMDs.

- Preserves Roth funds for heirs, who can inherit them tax-free under certain conditions.

2. Proportional withdrawals

Instead of following a strict order, proportional withdrawals pull money from all account types based on their percentage of your total savings.

For example, if:

- 50% of your savings are in a traditional IRA

- 30% are in a Roth IRA

- 20% are in a taxable account

Then each withdrawal would be taken in the same proportion:

- 50% from the traditional IRA

- 30% from the Roth IRA

- 20% from the taxable account

A proportional method spreads out tax liability evenly over time, rather than deferring all pre-tax withdrawals until later in retirement, potentially reducing your total tax liability

|

Which is the “best” strategy?: Frankly, a personalized one. It should factor in your tax situation, income needs, and retirement goals. That’s exactly why we recommend speaking with a wealth advisor — schedule a free consultation and we’ll help you model different scenarios, so you can determine your best path forward. |

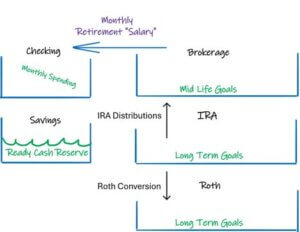

Visualizing Your Withdrawals: Retirement Cash Flow Waterfall

Withdrawal strategies and guardrails are inherently technical and, as a result, often difficult to visualize in day-to-day life. One way to conceptualize your retirement income is the retirement cash flow waterfall: a method for structuring your accounts and setting up flows for distributions.

1. Investment Accounts: The Source of Your Retirement Salary

Retirement assets are typically spread across brokerage accounts, IRAs, and Roth IRAs — ideally held with one custodian for simplicity. Within your investment accounts, you’d initiate a recurring sell order to convert holdings into cash, sending a monthly distribution to your checking account to fund your living expenses. From that monthly distribution, you can have federal and state taxes automatically withheld.

2. Your Bank Accounts: Your Readily Accessible Cash

These are your personal operating accounts: checking (one-to-two months of expenses) and high-yield savings (six–month cash reserve).

- Checking Account: Receives direct deposits from automatic investment distributions, acting as your monthly retirement “salary.”

- High-Yield Savings Account: Serves as a buffer for larger expenses (e.g., car purchase, home remodel, travel) so that you don’t need to sell investments at an inopportune time or trigger large tax events.

3. Retirement Guardrails: Managing the Flow Rate

With your accounts in place and automatic distributions enabled, the next objective is managing your flow rate within your guardrails. For instance, we’ll assume your guardrails are 4% and 6%.

If withdrawals exceed 6%, you’d reduce deposits into savings and reassess spending.

If withdrawals drop below 4%, you could direct more distributions into savings, building an accessible, guilt-free cushion for future spending.

This approach ensures that, just like you dollar-cost averaged into the market while saving, you are now dollar-cost averaging out in a controlled, tax-efficient way — avoiding large one-time sales by gradually pulling from investments.

4. Adapting for RMDs and Roth Conversions

You’ll likely also have upstream and downstream flows between your investment accounts. For instance, once you reach RMD age, IRA distributions can be reinvested in a brokerage account. In the same vein, strategic IRAto- Roth conversions could help you shift assets into taxfree accounts at favorable tax rates.

Key Takeaways

- Your withdrawal strategy affects how long your savings last. Without a structured approach, you risk depleting your assets too quickly or paying unnecessary taxes.

- Taxes matter — sequence your withdrawals strategically. The order in which you draw from taxable, tax-deferred, and tax-free accounts impacts your total tax burden and retirement income.

- RMDs can create unexpected tax spikes. Planning ahead — by making early withdrawals or Roth conversions — can prevent large, forced distributions later.

- You don’t have to follow conventional wisdom. While many retirees withdraw from taxable accounts first, proportional withdrawals can reduce long-term tax liability.

- Withdrawal strategies should adapt over time. As market conditions, tax laws, and your personal situation evolve, reviewing and adjusting your approach is integral to sustainability.

A deliberate withdrawal strategy can provide the income you need while preserving your wealth for the long haul. In the next chapter, we’ll explore the true cost of medical expenses in retirement, strategies to fund long-term care, and how to protect your financial future from rising health care costs.

See If You're a Good Fit

Your responses go directly to a senior member of our team, who’ll guide the next steps toward a personal conversation. No automation. No sales pressure.